FOTON NEV REPORT 2020.09

40 units of Foton AUMARK iBlue light duty truck was delivered to COFCO Coca-Cola, opening a new stage of electric development for green freight in the capital

Customization products contribute to efficient city logistics

With its large capacity battery of 104.7 °, combined with the braking energy recycle and lightweight body, AUMARK iBlue new energy logistics vehicle has a measured endurance of more than 200 km on full load, and can be fully charged within about 2 hours by using special charging pile. Its excellent performance has been highly recognized by COFCO Coca-Cola. The excellent long endurance and high reliability of Aumark iblue will greatly meet COFCO Coca-Cola's transportation needs from storage centers to distribution points or large supermarkets, and greatly improve the efficiency of the company's overall operation.

Part two

AUMARK NEV HIGHLIGHTS

Equipped with CATL battery, Foton launched new electric light duty truck

In response to the acceleration of the new energy transformation of urban distribution logistics, Foton united CATL launched the professional 4.5T pure electric light duty truck, which is equipped with CATL 81.14C lithium iron phosphate battery.

CATL, as the world's leading research and development of lithium ion battery manufacturing company, with higher energy density, stronger reliability of the battery, become the perfect partner with Foton, which committed to the lightweight, intelligent and has many years of commercial vehicle technology accumulation. They work together to meet in compliance, sufficient range, vehicle reliability requirements of customers.

Long mileage, efficient fast charging:

The new Foton 4.5T pure electric light duty truck is equipped with CATL 146.7Wh/kg ultra-high system energy density battery pack, which ensures the vehicle's constant speed 300km range and can be fully charged with 80% power within 50 minutes. Under the actual test of urban road conditions in Beijing, 6T full speed driving of the vehicle can still reach the standard driving mileage, meeting more than 90% of the needs of urban distribution logistics scene.

❒ High safety, high reliability:

The battery pack has passed 273 rigorous tests, such as high temperature, extrusion, impact, vibration, seawater immersion, high and low temperature impact, etc. Meanwhile, it is also equipped with standard air-cooled/liquid cooled dual-separation heat management system, which can provide a real super-long quality guarantee of up to 6 years and 300,000km.Equipped with ABS integrated control system, EBD electronic braking force distribution and other electronic auxiliary functions, it improves the active safety and driving comfort of the vehicle. The vehicle has gone through the high temperature and high cold limit test to ensure the safety of customers.

❒ Compliance guarantee:

Equipped with high energy density technology, the battery system of CATL weighs only 553kg. Combined with the light weight body of Foton Light duty truck, the vehicle has a total reassembling weight of 2970kg, which ensures the high ground clearance and high passing ability of the chassis of the vehicle, and can be easily and unlimitedly licensed. Under the premise of meeting the EKG index requirements and ensuring the subsidy for users, the 1.5T cargo weight demand of urban distribution logistics is guaranteed.

Part three

Global NEV Report

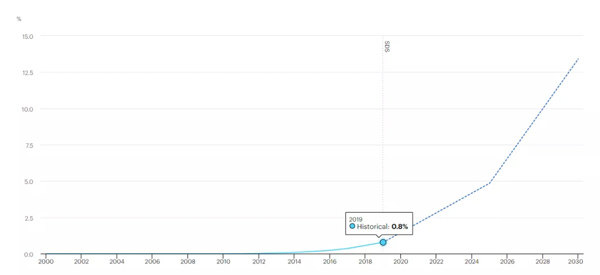

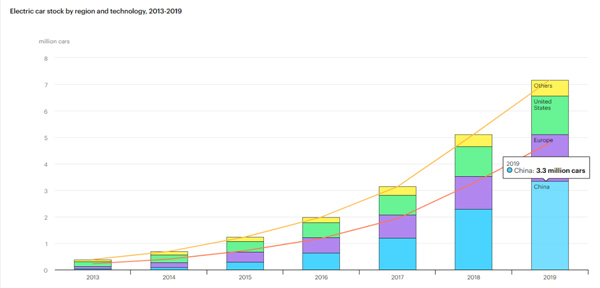

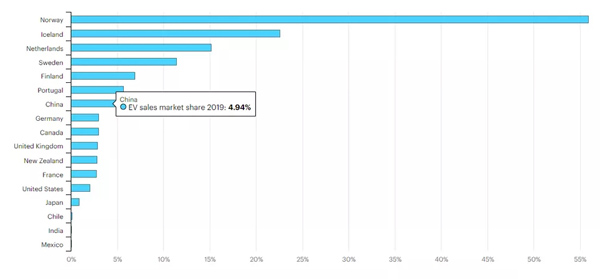

Electric car sales topped 2.1 million globally in 2019, surpassing 2018 – which was already a record year. Sales rose 6% from 2018, following several years of over 40% annual electric car sales growth. The 2019 increase is embedded within the third year of global car market contraction, and the global electric car market share reached a new record of 2.6%, up from 2.4% in 2018 and 1% in 2017. The electric car stock therefore increased 40% year-on-year in 2019, indicating strong sustained EV sector development after annual successes since 2016 and a positive outlook for attaining the 36% average annual stock growth needed to reach the SDS target by 2030. China was the world's largest market (1.06 million electric cars sold in 2019), followed by Europe (560 000) and the United States (326 000); these three regions accounted for over 90% of all sales in 2019. Norway continues to have the highest market share for sales (56% in 2019), followed by Iceland (23%) and the Netherlands (15%). Battery electric cars (comprising battery electric cars and plug-in hybrid electric cars) made up a larger portion of electric car sales (almost three-quarters) in 2019. Progress in decarbonizing the power sector will accelerate the CO2 emissions reduction benefits of EVs.

Technology developments and support policies sustained electric car appeal in 2019, but reductions to direct subsidies in key markets led to slower global growth

With electric cars making up 2.6% of global car sales and about 1% of global car stock, and with market and technology progress being made in electrification in non-car modes, EV rollout is expanding quickly. Indeed, electric car stock increased 40% year-on year in 2019.

Although ambitious policy announcements have been critical in stimulating the transition to electric mobility in major vehicle markets in recent years, direct subsidy reductions and phase-outs in 2019 indicate a continuing shift to policy approaches that rely more on regulatory and fiscal measures to underpin the deployment of EVs – including increasing reliance on supply-side measures such as zero-emission vehicles mandates and fuel economy standards.

While 2019 was marked by continuous technology announcements in EV model diversification and battery performance progress, policy changes in key markets led to electric car sales stagnating in China (-2%, following a purchase subsidy reduction in June 2019 after which sales decreased); declining 10% in the United States; and accelerating in Europe (+50%) relative to 2018.

The global stock reached 7.2 million in 2019, with China claiming 47% of all electric cars on the road – up from just 8% in 2013.

With rapid growth in electric car sales over the past decade, electric cars make up about 1% of the global car fleet today. In the Sustainable Development Scenario (SDS), 13% of the global car fleet is electric by 2030, requiring annual average growth of 36% per year between 2019 and 2030.

Battery electric vehicles, accounting for roughly three-quarters of electric car sales globally, were particularly successful in many markets in 2019, with rises of 80% across Europe as a whole and 43% in Canada, and stable sales in China and the United States, leading to global annual sales growth of 14% in 2019.

Meanwhile plug-in hybrid sales dropped 11%. Plug-in hybrid EV models became widely available on the market around 2012 and by 2019 they made up roughly one-third of the global electric car stock. The primary markets continue to be China (40% of global sales) and Europe (36%). Plug-in hybrids made up 36% of electric cars sold in Europe in 2019 and 21% China.

While direct purchase incentives are being reduced in the United States and China, regulatory mechanisms are gaining importance in China and the European Union

About 25% of all two-wheelers on the road are electric, and they are mostly in China (over 95%), India and ASEAN countries. Electric micro-mobility is also becoming more popular in many large cities owing to shared bicycle and foot-scooter schemes.

The global market for electric buses has declined since a spike in sales in 2016. In 2019, new electric bus registrations numbered around 75 000, down 20% from 93 000 units in 2018. There were about 513 000 electric buses worldwide in 2019, up 17% from 2018.

The primary electric bus market is still China, which accounts for 95% of the market and has a number of cities with fully or near-fully electrified bus fleets. But increasing numbers of electric buses are being procured in Europe, India and Latin America. In fact, the city of Santiago de Chile owns the largest electric bus fleet outside of China.

Most medium- and heavy-duty electric trucks on the road are in China, where the sales rose over 6 000 units in 2019. In Europe, a group of original equipment manufacturers (OEMs) has delivered electric medium-freight trucks to selected fleet operators for commercial testing.

Even shipping and aviation are making electrification progress, as several electric ships are now in operation in Europe and China and the first all-electric commercial passenger aircraft flight took place in December 2019, when a retrofitted seaplane took a 15-minute flight from Vancouver, British Columbia. Cold-ironing and electric taxiing in particular are potential avenues for the gradual electrification of these two hard-to-abate sectors.

03

While direct purchase incentives are being reduced in the United States and China, regulatory mechanisms are gaining importance in China and the European Union

Several key regions are ramping up policy efforts to electrify various transport modes. The vast majority of car markets offer some form of subsidy or tax reduction for the purchase of an individual or company electric car, and 60% of global car sales are covered by China’s NEV mandate, the EU CO2 emissions standard or a ZEV mandate (in selected US states and Canada).

In April 2019, the European Union approved a new fuel economy standard for cars and vans for 2021‑30 and a CO2 emissions standard for heavy-duty vehicles (2020‑30), with specific requirements or bonuses for EVs. Previously, the standards targeted the year 2020 for compliance with emissions standards for light-duty vehicles of 95 gCO2/km, which has contributed to the success of EVs in Europe in recent years. Aggressive targets for the target year of 2030 will continue to favour the adoption of EVs. In addition, a revision of the Clean Vehicles Directive in 2019 aims at accelerating the adoption of electric buses (and other publicly procured vehicles) in EU countries, setting specific targets for 2025 and 2030.

China updated its fuel economy standard for light-duty vehicles for 2021-25 in January 2020. The standard, to be phased in gradually from 2021, sets a 4 l/100 km target for the country's new vehicle fleet in 2025. Through a fuel economy credit scheme, OEMs are obliged to reach that target, or cover any credit deficit through transfers, past carry-overs, or NEV credit surplus.1 A separate standard on EV efficiency sets a voluntary target on energy consumption based on weight classes. China has also scaled back subsidies for EV purchases and for battery manufacturers, but maintained its zero-emissions vehicle mandate scheme that sets minimum production requirements for the car manufacturing industry, tightening requirements for EVs to be able to access credits.

India is ramping up EV support through phase 2 of its Faster Adoption and Manufacturing of Electric Vehicles scheme, focusing on two-wheelers, fleet vehicles and buses. Other countries with increasing policy activity to support EVs are Canada, Costa Rica, Chile and New Zealand.

In 2019, more than 90% of global car markets in terms of sales (encompassing more than 50 countries) had EV incentives in place, although gradual phase-out at the national level has begun in key markets such as China and the United States. Support policies for charging infrastructure were in place for 80% of the market. However, other policies also impact the EV market, such as building codes for the installation of charging infrastructure and demand-response policies for grid services.

Given the strategic relevance of batteries for industrial development and the clean-energy transition, governments are supporting investments in battery manufacturing facilities and innovation in battery technology.

04

Battery technology developments continue to advance with positive achievements and a promising outlook

Automotive batteries are a major cost component of EVs. In 2019, the average sales-weighted lithium battery price fell 13% from 2018, to USD 156/kWh, down from more than USD 1 100/kWh in 2010.

With battery production required to increase about eighteen-fold by 2030 in the SDS, significant battery cost reductions can be expected through the conjunction of increasing battery pack size, battery chemistry changes and economies of scale thanks to larger manufacturing plants.

Growth of the Chinese – and global – automotive battery market is instrumental to prompt battery manufacturing capacity expansion and reap the benefits of economies of scale.

While most production is currently still sourced from relatively small plants (capacities of 3-10 GWh per year), several recent production capacity expansion announcements point to an increase in plant size as well as to new entrants in the automotive battery market, adding to rising capacity utilization rates of existing plants.

OEMs have set a wide range of targets to supply the vehicle market with EVs. The number of EV models is expanding rapidly, with carmakers having announced dozens of models in various sizes, most of them coming online in the first half of the 2020 decade.

Views:0

- FOTON Pakistan Delivered 3 Express Logistics Vehicle to DHL 2022-04-12

- CP FOTON’s Dealer Summit & AUMARK FLEX Launch Ceremony Held in Thailand 2022-04-12

- 328 Units!China’s First Largest Automatic Heavy Truck Export Order to Colombia 2022-04-08

- AUMAN EST-M Rolled off the Line at Foton Pakistan Factory 2022-04-03

- 400 Units of FOTON AUMAN Trucks Delivered to an Int'l Brewery Group of Nigeria 2022-04-01

- FOTON Mexico Passed the ISO9001 International Quality System Certification 2022-03-30

- FOTON Got First RCEP Certificate of Origin to Malaysia Issued by Beijing Customs 2022-03-23

- FOTON and Piaggio Group’s 10000TH NP6 New Porter Built at Italian Plant 2022-03-12

- FOTON Donates Mobile Service Vehicle to Boost Healthcare in Pakistan 2022-03-08

- FOTON AUMAN Impressed the World with Powerful Backing for "Dual Olympic City" 2022-02-11

Submit Your Requirements, We Are Always At Your Service.

- BYD Stopped the Production of Fuel Vehicles

- Geely Began Test Runs of Green E-methanol Vehicles in Danmark

- 2022 SANY Global Dealer Summit Was Held Successfully Online

- BYD and Shell Partner on EV Charging across China and Europe

- Daimler Truck Significantly Increase Sales, Revenue and Net Profit in 2021

- Scania Year-end Report January-December 2021

- Hyundai Motor and Iveco Group Sign MOU to Explore Future Collaboration

- GAUSSIN Enters China, the Largest Truck Market in the World

- Over 1,200 Hydrogen-powered Vehicles Deployed for the Beijing Winter Olympics

- Chinese New Year Holiday Closure Notice

- China's Truck Exports Grew by 30% YOY to 63490 Units in January-February

- China's New Energy Heavy Trucks Grew Despite an Overall Slump

- Heavy-duty Truck sales in China Fell by 54% to 54,000 units in February

- SINOTRUK Achieves Sales of 27,725 Vehicles in January, 2022

- China’s Domestic Tractor Sales Exceed 40,000 Units in January

- 2021 JAC International Pickup Export Performance

- JAC Achieved a Great Result in 2021

- China's Truck Export in 2021 Reached a 10-year Peak

- Heavy-duty Truck Sales in China Fall 57 Percent on Year in January

- China Recorded Sales of 645000 Tractors in 2021